HOW BRAZIL USED PSYCHOLOGY TO END HYPERINFLATION, and why didn't the Trump tax cuts lead to inflation?

|

| Image by author, “Christ the Redeemer” image from Flickr, Creative Commons license |

I suspect that when most people think of the word “economics,” images of spreadsheets and mathematical formulas dance in their head. In reality, if you go to your local university, economics isn’t in the math department or even the business school. It’s in the social studies department, alongside philosophy, sociology, and history. Economics is the study of how people, governments, and businesses interact with wealth. In other words, it’s the study of human behavior. So thinking about it in those terms it’s not surprising that Brazil was able to solve their hyperinflation with psychology.

Now You See It, Now You Don’t

Money is basically a mass delusion we’ve agreed to accept. Early people didn’t need money, they simply traded what they had for what they needed. Once civilizations became larger and more complex, bartering no longer met their needs. Coins made of gold and silver started taking the place of trading goods and services. This system required everyone to agree the coins had value since they didn’t serve any other function. Still, at least the coins had intrinsic value, people could melt them and sell the metal if necessary. This system seemed to make instinctive sense and continued for thousands of years.

However, the ever-growing need for more currency and practical issues of using precious metal as the medium of exchange eventually demanded new solutions. Paper money was the answer to this problem, but was viewed with suspicion. It had no value outside of people’s trust in the institution that issued it. Over time the practical advantages of paper money won the day, yet today we don’t even have that. The vast majority of money is a series of 1s and 0s on a bank server. We need to have faith that those numbers have value in the real world. That we can convert those 1s and 0s in computer codes into actual physical products.

Hyperinflation destroys that illusion. Once hyperinflation begins we may have the money our bank indicates, but it no longer has the power to purchase real world things. In theory, inflation isn’t that complicated. When supply is high and/or demand low there is low inflation, or even deflation (falling prices). Conversely, when supply is low and/or demand is high, inflation is the result. A government deciding to stimulate their economy by printing a bunch of new money is a classic example. It creates demand because people have money, however, it doesn’t create supply. The result is usually out of control inflation or hyperinflation.

The Psychology of Inflation

Once hyperinflation starts, it’s often difficult to get under control. Businesses have to pay more in wages so their employees can live. This requires that they raise prices in order to cover the higher wages, which in turn requires the employees to need even higher wages. It can quickly turn into a self-perpetuating cycle. However, when you break down the actual dollars and cents of it, the math doesn’t fully account for hyperinflation. This is where psychology comes into play.

A key factor in inflation is expectation. When there’s high inflation businesses are likely to raise prices based on the expectation of inflation. This is the part of the equation that is so difficult to break. Governments usually raise interest rates to decrease the money supply, thus lowering demand and inflation. But if people still expect prices to rise, it’s likely prices will continue to increase. The combination of high interest rates and high inflation can cause an economy to spiral downward leading to increased unemployment. This is known as stagflation (stagnation plus inflation).

Stagflation and Nixon

Image by author, data source BLS and St. Louis Fed.

This is what happened in America in the 1970s and early 80s. A series of policies enacted by President Nixon planted the seeds of inflation that sprung to life during the Ford and Carter administrations. America’s unique position as the only major economy unscathed by World War 2 led to decades of both low unemployment and low inflation in America. By the late 1960s that began to change. In 1970 unemployment had risen to over 6% with virtually zero economic growth. To boost his chances of re-election, Nixon embarked on a series of policies that risked inflation, but boosted the economy in the short run. These included abandoning the gold standard, attempts to set price and wage controls, and pressuring the Federal Reserve to lower interest rates instead of raising them to prevent inflation.

In the short term these measures worked. 1972 saw decreased unemployment and strong economic growth which led to Nixon’s re-election that year. However, these policies set in motion a series of market reactions over the next decade that led to the highest unemployment since the Great Depression and the highest inflation ever recorded. It was only when the Federal Reserve Chairman Paul Volcker raised the interest rate banks charge each other to borrow money to 18% that inflation finally started coming down. As a point of comparison, the current rate is 0.25%. Through careful management by the Federal Reserve, we’ve managed to maintain a prolonged period of low inflation ever since. This despite the normal cycle of recessions and expansions that have occurred over the last 40 years.

High inflation is just insidious to an economy. If inflation is 10%, a bank will lend money at a higher rate to prevent being paid back money at an effective loss. These high interest rates make it difficult for businesses to expand or for people to make large purchases. It’s a constant weight on the economy that stifles growth. It causes retirees and people on fixed incomes to see their purchasing power diminish each month. In most cases the only solution is some combination of even higher interest rates or higher taxes to decrease the money supply like Paul Volcker instituted in the late 70s. It’s a painful process.

Brazil’s Hyperinflation

Nowhere was this more apparent than in Brazil. They alternated between high inflation and out of control hyperinflation for decades. Beginning in the 1950s they made a rapid effort to modernize and industrialize the country. This included building a new capital city (Brazilia), creating a new system of highways and many other infrastructure and cultural building projects. However, when they began this program they didn’t have the mature economic controls in place to manage their finances. Brazil financed much of this building by simply printing more money. Out of control inflation was the inevitable result.

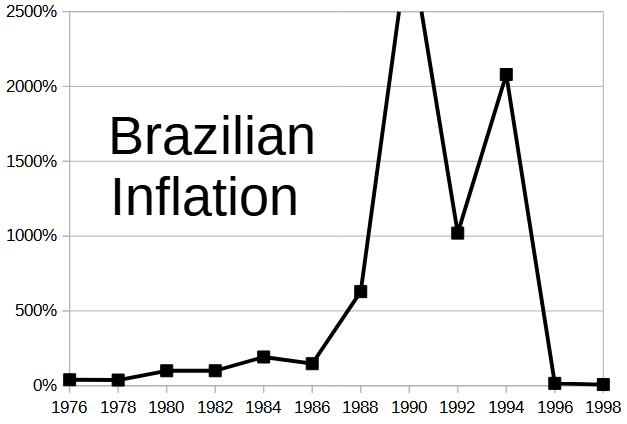

Over time Brazil attempted to correct these early deficiencies by creating a central banking system and establishing a more sustainable system of taxation. These efforts helped but never fully solved the problem as their inflation continued to bounce between 30% and 100% through the 1970s. In the 1980s these past failures began to catch up with the Brazilian economy. From 1981 to 85 the rate of inflation more than doubled from 100% to 226%. It then nearly tripled in the next 3 years up to 629%. Finally, from 1989 to 1994 full hyperinflation gripped the country with an average of over 2000% annual inflation.

Image by author

Prices in the stores increased nearly every day. People would try to stay ahead of the guy coming down the aisle in the grocery store increasing the prices. Imagine going to the store and buying a gallon of milk for $3 in January. Next month it’s $8, the following month $21.50, in April it’s $58, then $155, finally 6 months into the year it’s $415 per gallon. They were living with these conditions for years.

The Failed Solutions

With a currency that was virtually worthless, economic growth was virtually impossible. Brazil had managed fairly consistent growth despite the inflation over the previous decades. But from 1988 to 1992 the GDP only grew an average of 0.2% per year. Brazil’s government wasn’t blind to this situation and successive Presidents launched plans to stabilize the currency. Most of these plans involved a shock to the system by freezing wages and prices for a period of time to break the inflationary cycle.

Theoretically this idea seems like it might work, however in fact these plans always produced winners and losers. Because prices and wages increased at different times, people who had just received a raise when wages were frozen were in a good position. However, those who were about to get a raise were stuck with low wages. The government would then need to make adjustments but was unable to do so in a timely manner and the whole thing would fall apart. Each new plan tried to account for these problems, but new unexpected problems would arise, sinking the effort. The end result was an impression that the government was powerless to fix the problem.

And We Have A Winner

Finally in desperation a new Finance Minister approached a team of economists and gave them a free hand to develop and implement a plan to address the hyperinflation. It was widely acknowledged that much of the problem lay in the public’s expectation that prices would rise, yet the forced freezing of prices hadn’t worked. These economists proposed a method of breaking that expectation without an artificial price freeze. They mandated that stores list prices in both the old currency but also a new non-circulating currency called the Real. The Real was basically a fake currency. This new currency was kept at a stable rate. So that gallon of milk that cost $3 last month would still cost consumers $8 the following month, but alongside the purchase price, the price in Reals would still say $3.

Eventually, people embraced the idea of the Real and started referring to prices in Real even though products were still purchased using the old currency for an inflated price. Finally, after several months of this, the government officially switched currencies and replaced all the old money with the new Brazilian Real. Because people had come to accept that prices in Reals were stable there was no rush to increase prices. And just like that hyperinflation ended. Of course, this only worked because other efforts to address the underlying problems were also instituted. It also didn’t solve all of Brazil’s economic problems, but it did end the hyperinflationary cycle.

So, Where’s the Inflation Today?

For both the stagnation in the U.S. in the 1970s and Brazil’s hyperinflation of the 1990s increased money supply was at the root of the problem. Brazil printed money to fund its infrastructure program and Nixon pressured the Federal Reserve to cut interest rates when they should have raised them. The question this raised in my mind is, why didn’t the Trump tax cuts cause inflation? These tax cuts put billions of dollars into the economy when it already had strong growth. Normally that’s a recipe for economic growth, but also inflation.

The bulk of the tax cuts that went into effect on January 1st, 2018 went to corporations. The Trump administration expected them to reinvest this windfall back into the company to spur growth. What actually happened is corporations went on a stock buyback binge. Stock buybacks increased 55% in the first year after the tax cuts and continued at that rate for the first half of 2019. Corporations did this because it drives up share prices. If there are fewer shares available, the price of each share will be higher.

From mid-2019 to mid-2020 the rate of stock buybacks went down, but corporate cash on hand surged 89% in one year. When businesses use money for stock buybacks or put it in the bank it doesn’t stimulate the economy. As a result, both economic growth and inflation remained unchanged. The net result of the Trump tax cut was corporations and their major shareholders got richer. Most of the tax cuts never filtered down into the overall economy.

Source St. Louis Federal Reserve

Expectations also played a role, but in a positive way this time. Because of America’s track record of low inflation the expectation was that prices would remain stable. Consumers and businesses acted according to this expectation. As a result, even the money that did filter into the economy didn’t immediately cause increased prices.

Today, in the wake of disrupted supply and demand caused by COVID-19, and an unprecedented amount of government stimulus, economists are divided on their economic predictions. The real wild card is business and consumer expectations. Expectations will drive economic activity more than the data. Economists like stability and predictability, but these are extraordinary times. In the end it’ll be the millions of little decisions made by America’s businesses and consumers that will determine how this plays out.

Comments

Post a Comment